Commentary

The 4.9% unemployment rate has become a cruel joke, considering the real facts. Today, fewer Americans have full-time jobs than in 2007, and the size of the workforce is down to numbers we haven’t seen since the 1970s. GDP is anemic, and numbers that were once regarded as needing “emergency attention” are being taken as a “pleasant surprise.”

Two of the biggest economic factors for economic growth include student debt and car loans, which are looking very close to the subprime mortgage crisis we saw in 2006. John Rubino, of DollarCollapse.com, pushes past the fake Keynesian paradigm and digs into the real numbers that would suggest the rosy economy is a major illusion.

I couldn’t agree more with him… What we are being spoon-fed from the mainstream is complete garbage, and people will have to wake up soon enough to the realities of what the economy is facing. For many, the bubble burst will come as a surprise, but those who are in the know will be the ones best able to cope with the massive shift in what we all perceive as “normal.”

Best Regards,

Kenneth Ameduri

Chief Editor at CrushTheStreet.com

Main Article – Source

Bad — But Better Than What’s Coming

Author: John Rubino

Talk about diminished expectations. This morning’s estimate of 1.4% Q4 GDP growth is being hailed as a pleasant surprise. Which is odd, considering that for most of the past century a number this low would have been seen as weak enough to require emergency action.

And that’s just the headline number. Dig a little deeper and the picture — at least when viewed through a non-Keynesian lens — is of a system in crisis. Consider:

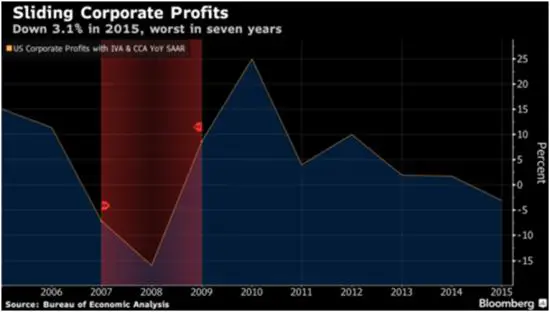

Corporate profits are, as today’s Bloomberg puts it, sliding.

Meanwhile (also from Bloomberg),

A firm labor market and low inflation encourage households to keep shopping. Today’s fourth-quarter growth figure reflected more spending on services, particularly on recreation and transportation. “It’s really U.S. consumers who are powering the global economy forward at this point,” said Gus Faucher, an economist at PNC Financial Services Group Inc. in Pittsburgh.

But if companies are earning less money, how likely is it that they’ll step up hiring going forward? Not very. And since today fewer Americans have full time jobs than in 2007 (making the current stellar 4.9% unemployment rate look like a cruel joke) a new round of mass layoffs will make the job market even more dire for anyone hoping to support a family with full-time work.

“If profits remain depressed, the prospects for capex and hiring will come under greater pressure,” Sam Bullard, a senior economist at Wells Fargo Securities LLC in Charlotte, North Carolina, wrote in a research note.

What are the chances of profits remaining depressed? Pretty good, considering that two of the big growth drivers of the past few years have been student debt and car loans. The former is, as everyone by now knows, at levels that consign a whole generation of kids to life in their parents’ basements — not a recipe for robust consumption.

Car loans, meanwhile, are starting to look like subprime mortgages circa 2006:

Unpaid subprime car loans hit 20-year high

(CNN Money) – Americans with lower credit scores are falling behind on auto payments at an alarming pace.The rate of seriously delinquent subprime car loans soared above 5% in February, according to Fitch Ratings. That’s worse than during the Great Recession and the highest level since 1996.

It’s a surprising development given the relative health of the overall economy. Fitch blames it on a dramatic rise in loans with lax borrowing standards that have helped fuel the recent boom in auto sales. More Americans bought new cars last year than ever before and the amount of auto loans soared beyond $1 trillion.

Fitch points out that the subprime end of the market is where there’s increased competition to peddle loans. The ratings firm flagged an increase in loans to “borrowers with no FICO scores,” lower downpayments, and extended term lending.

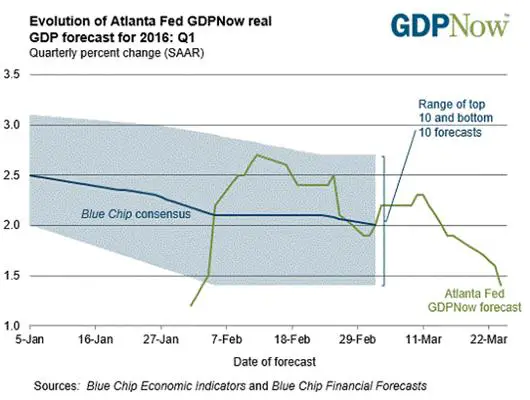

Toss in contracting global trade, turmoil in Europe and Latin America, and a grinding multi-month decline in US manufacturing output and the year ahead doesn’t look any better. Here’s the Atlanta Fed’s GDPNow measure of current growth, which shows a huge drop in just the past month:

What does all this mean? Very simply, if you borrow too much money life gets harder and the things that used to work stop working. For a country, lower interest rates no longer induce businesses and individuals to borrow and spend, and government deficits no longer translate directly into more full-time private sector jobs. Growth slows, voters get mad, politics gets crazy, and generally bad times ensue. The only question is why this is a surprise to the people whose choices brought us to the edge of the abyss.

http://dollarcollapse.com/the-economy/bad-but-better-than-whats-coming/