The new edition of In Gold We Trust is out. It is a globally read, outstanding report, full of unique insights for investors. The report analyzes montary policies, the financial system, the economy, and the role of precious metals in all those areas.

The report is written by Ronald Stoeferle, managing partner at Incrementum AG in Liechtenstein, a global macro fund influenced by the Austrian School of Economics.

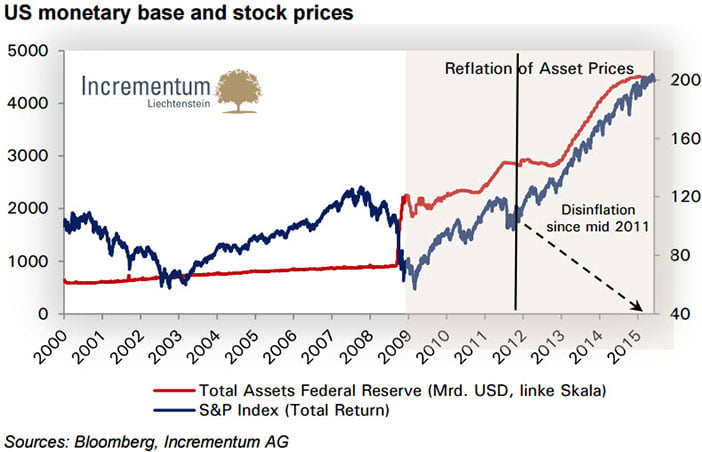

The Wealth Effect

The key topic of the report is the global over-indebtedness. The debt situation in many regions of the world is unsustainable. The idea that “growing out” of overindebtedness would be possible, seems a highly unrealistic expectation, as there is no realistically achievable combination of tax rates and growth rates in most countries that would allow for a sustainable reduction of the extant debt burdens.

A consistent, drastic austerity policy shouldn’t be expected. Southern European countries are an example showing the democratic limits with respect to austerity policies. Zero interest rate policies are a major pillar supporting high debt ratios and are even increasing the incentive to amass additional debt.

The economic cycle appears quite mature by now. After 2008, money supply inflation has been employed in unprecedented fashion in order to artificially boost the economy. Especially the increase in economic activity in the US in recent years is attributable to the illusion of growing prosperity through the so-called “wealth effect”.

This can be illustrated by dividing the reflationary trend after 2008 into two segments: pre and post 2011.

While from 2008 to 2011 the prices of both stocks and commodities were driven higher, a disinflationary trend in commodity prices has taken place since 2011. Since then, money supply inflation primarily induced asset price inflation (think of stocks). This phase has culminated in a disinflationary tsunami in 2014. A strengthening US dollar exerting deflationary effects once again delayed the probability of a rate hike and left the much-desired zero interest rate environment in place, benefiting stock markets.

However, a trend change has to be underway. Over the coming three years, a paradigm change is likely to become evident in the markets, quite possibly including rising inflation. The following scenarios have the highest probability:

Scenario I: The current economic cycle nears its end and the fairy tale of a self-sustaining recovery is increasingly questioned by market participants. This leads to a significant devaluation of the US dollar relative to commodities, since the Fed – as it has stressed time and again – will once again employ quantitative easing or similar interventions if occasion demands it. In this case gold would benefit significantly from wide-ranging repricing in financial markets. A stagflation-type environment would become a realistic alternative in this scenario, something that is currently on almost no-one’s radar screen.

Scenario II: Rising yields lead to an increase in credit creation and an increase in money velocity (= decline in the demand for money). Economic activity picks up, is however accompanied by accelerating price inflation.210 In this scenario, both financial assets (with the exception of bonds) and real assets (such as gold) would benefit in nominal terms.

Scenario III: The system hasn’t become any healthier since 2008, but has in fact become more fragile in many respects. Due to further concentration in the banking sector, the balance sheets of the largest banks have grown enormously. The volume of outstanding derivatives has continued to grow, with many off-balance sheet positions. In addition, the geopolitical situation hasn’t been this tense since the end of the cold war. The probability of a “black swan” event striking is therefore in our opinion higher than it has been in a long time. In this type of scenario, gold would likely emerge as a beneficiary as well.

In each of those three “most likely scenarios“, gold will remain in a secular bull market. In light of the perspective discussed above, In Gold We Trust sets a time horizon of three years for its long term gold price target of USD 2,300.