While events last Friday were overshadowed by yet another major terrorist attack, the financial players of Wall Street did have something to smile about. The S&P 500 index only moved up 0.38% but it was enough to secure the title for the (thus far) best week in the markets for 2015, which ultimately gained 3.27%. The major indices were buoyed by the retail sector, which finally began to show signs of life after what has been on paper a fairly dismal series of earnings performances. But underneath all the hoopla, a quiet recovery has been taking place in the emerging markets.

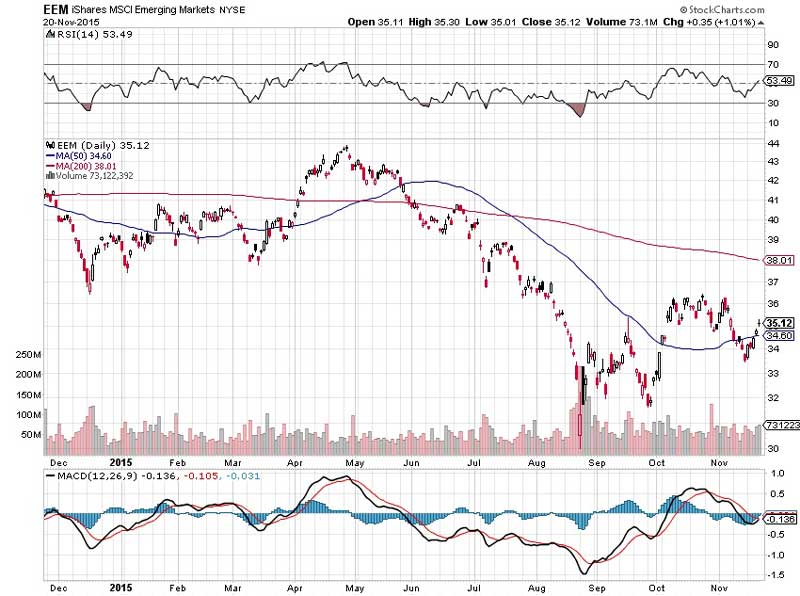

The benchmark iShares MSCI Emerging Markets Index (NYSEARCA:EEM) — which covers a significant portion of Asian financial services and technology sectors — has been on a tear over the past several months, up more than 12% from its August 24 bottom. This shift in sentiment is in sharp contrast to EEM’s year-to-date loss of nearly -11%. With last Friday’s 1% move against the prior session, EEM has cleared its 50 day moving average.

On paper, this is all good and well. From a technical analysis perspective, however, it’s interesting to note that a “doji star” has formed in the charts on the Friday session, or a condition formed when a security’s opening and closing price are identical or nearly so. By itself, doji stars are neutral patterns — upon seeing one, there is a 50/50 chance that the markets can go either way. In this current context, a doji star formed after an uptrend, perhaps indicating indecision and a tight negotiation between the bulls and bears.

This pensiveness is both telling and somewhat alarming. For example, basic materials represent 7.52% of the EEM’s holdings. If the emerging markets are fundamentally improving, we would expect to see a boost in commodity production companies overall. Like the aforementioned doji star, we see evidence for and against this assessment.

Alcoa Inc. (NYSE:AA), the U.S. biggest producer of aluminum, tore up the markets last week with a near-9% swing up between November 13 and November 20. Does this suggest that the aluminum markets — progressively depressed by Chinese dumping — are coming back? It’s true that aluminum prices have risen recently, but if we look deeper, this is mainly a result of companies like Alcoa curtailing production — less supply equates to more demand. But the aggressive dumping of Chinese steel has yet to abate, which means that the aluminum sector is still vulnerable to sustained volatility. And Alcoa is really a flavor of the week — on a YTD basis, its shares are down almost 45%.

Ultimately, it’s not about picking on any one sector or region: all financial markets are subject to vulnerabilities, particularly because years of aggressive monetary stimulus has induced artificial demand attached to no real substance. The money that is distributed, along with “jobs” such as “social media management,” are existential — they are valid, but only from a source of circular affirmation.